Our private credit strategy is focused on delivering consistent monthly income with a strong emphasis on capital protection. The Fund invests primarily in high-quality, asset-backed lending opportunities which have produced stable returns across varying market conditions over the last 8 years. For the month of March, the Fund delivered a distribution yield of 0.73% which equates to an annualised return of 8.92% (net of fees). A key feature of the Fund’s approach is its use of warehouse funding structures, allowing the Fund to provide capital to specialist non-bank lenders while benefiting from first-loss protection, strict eligibility criteria and robust structural controls. Outlined below are how these structures generate income and manage risk for the Wentworth Williamson Stable Income Fund.

How Warehouse Funding Works

Currently all our investments in the Stable Income Fund are through investments in warehouse structures. When talking to some clients there has been some confusion over what a warehouse structure is, so we have included a description below to clear up any confusion.

What is a warehouse facility?

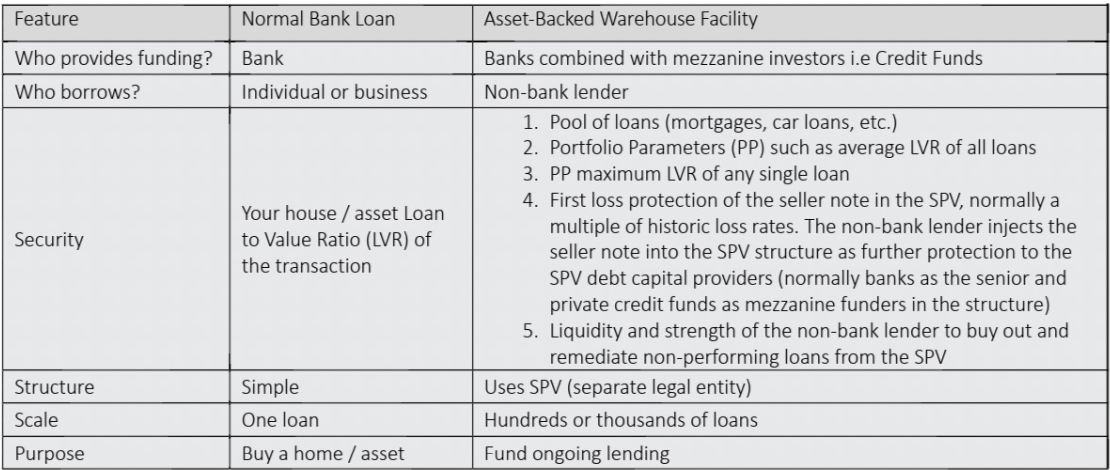

A warehouse facility uses a Special Purpose Vehicle (SPV), a separate legal structure set up solely to hold a pool of loans. All loans, along with their associated security and collateral, sit inside this structure rather than on a lender’s balance sheet. This approach is widely used by Non-Bank Financial Institutions (NBFIs) to fund lending activities. Examples of large Australian non-bank lenders include Pepper Money (residential property), MaxCap (development finance), Scottish Pacific (corporate loans), and Latitude Financial Services (personal and consumer finance).

At its core, a warehouse facility works the same way as a normal loan, but instead of one bank funding one loan, multiple funders share the funding across a large pool of loans. As a good example of how the structure works in practice, we compare the workings of a warehouse with a simple home loan from your bank. Many of you are familiar with a normal home loan with your bank. The bank funds it, holds your mortgage, and you repay the bank each month. That’s it. One lender. One borrower. One loan.

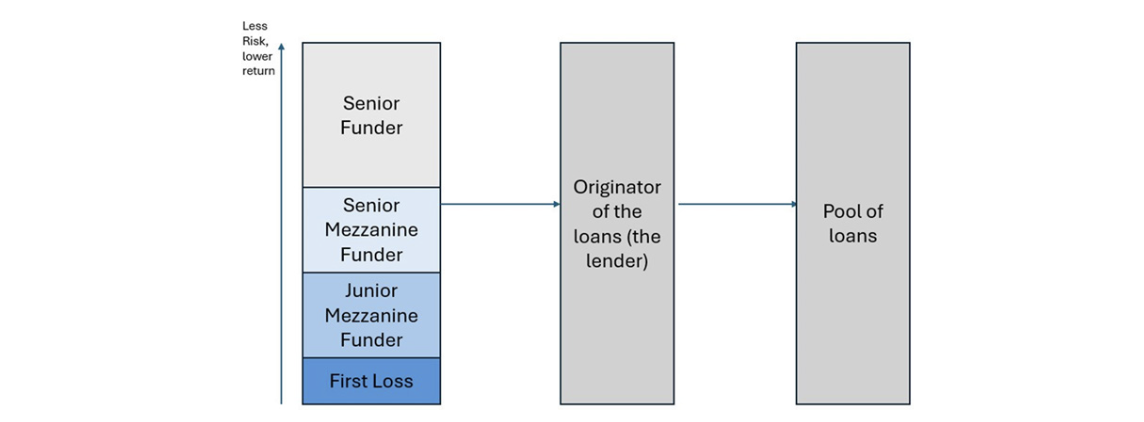

A warehouse facility follows the same economic principle, but instead of a single loan funded by one lender, multiple investors jointly fund a large pool of loans. These loans are held within the Special purpose Vehicle (SPV or “warehouse”), which is a stand-alone vehicle that does not operate a business, employ staff, or take operating risk. Its sole purpose is to:

• Own the loans,

• Hold the underlying security,

• Collect borrower repayments, and;

• Distribute cash flows to investors in a predefined order.

Traditional Bank Lending vs Warehouse Facilities

While the example uses a home loan for simplicity, the same structure is widely applied across asset-backed products with consistent cash flows, including residential mortgages, commercial property loans, equipment finance, personal loans, auto loans, and trade receivables. In practice, a warehouse facility typically includes multiple funders, each providing a different “Slice” of capital within the structure, and it holds a growing pool of loans rather than a single exposure. Cash flows are distributed according to a defined priority.

- Senior funders sit highest in the structure, receive priority repayment, and therefore earn the lowest returns,

- Mezzanine funders take progressively more risk in exchange for higher returns;

- and, the first-loss position (usually funded by the originating lender)absorbs losses first, similar to aborrower’s equity deposit in a home loan.

Any excess income (called a net income margin) after all funders have been paid flows to the loan originator (the NBFI). This structure allows non-bank lenders to efficiently fund and scale lending portfolios while providing investors with diversified exposure to a pool of secured loans.

Why Warehouse Structures are used

A warehouse allows loans to be funded as they are originated, while the portfolio builds and performance is observed. We use a warehouse because it gives investors comfort that:

- Loans are held separately from the NBFI’s day-to-day business, protected in a bankruptcy remote vehicle.

- Funding is backed by real assets and repayments, not just reliant on the NBFI’s BalanceSheet.

- The NBFI provides first-loss capital (normally a multiple of historical loss rates), meaning losses are absorbed before debt capitalproviders are affected. Furthermore, the warehouse is structured such that anticipated losses may be remediated by the warehousestructure cash flows over time or in some cases acquired out of the SPV by the non-bank lender themselves.

- Only loans that meet strict eligibility rules can enter the structure.

- Performance is monitored closely as the portfolio grows. Standard practice is the Trustee produces monthly reports which provide granular insight into the cashflows received from the pool of loans, arrears and compliance with portfolio parameters.

Why Warehouse Structures Benefit Investors

- Bankruptcy-remote protection: The loans sit in a separate trust, not with the non-bank lender.If the non-bank lender fails, the loans are still protected in a bankruptcy remote vehicle.

- Asset-backed security:Funding is secured only against the loan pool itself and all the collateral and securities of each loan, secured in the trust structure. Investors rely on borrower repayments and the security and collateral of the underlying pool of assets, rather than just the financial health of the lender.

- Diversification: The pooled structure also offers the lender significant diversification. In some cases, warehouse structures can hold thousands of obligors. The greater the diversity and size of the pool, the more likely the income earned from the performing loans can offset any losses from non-performing loans.

- First-loss protection from the issuer: The lender typically provides a junior or first-loss position. Losses are absorbed by the lender first, before mezzanine and senior investors are affected, providing a strong buffer.

- Strict controls on lending quality: Only loans that meet pre-agreed eligibility criteria can enter the warehouse. This prevents weaker or out-of-policy loans from being added.

- Ongoing monitoring and early intervention: The warehouse includes performance tests and limits. If loan performance deteriorates, new lending can be restricted or stopped to protect investors.

Simple structure diagram

How warehouse funding works (simple overview)

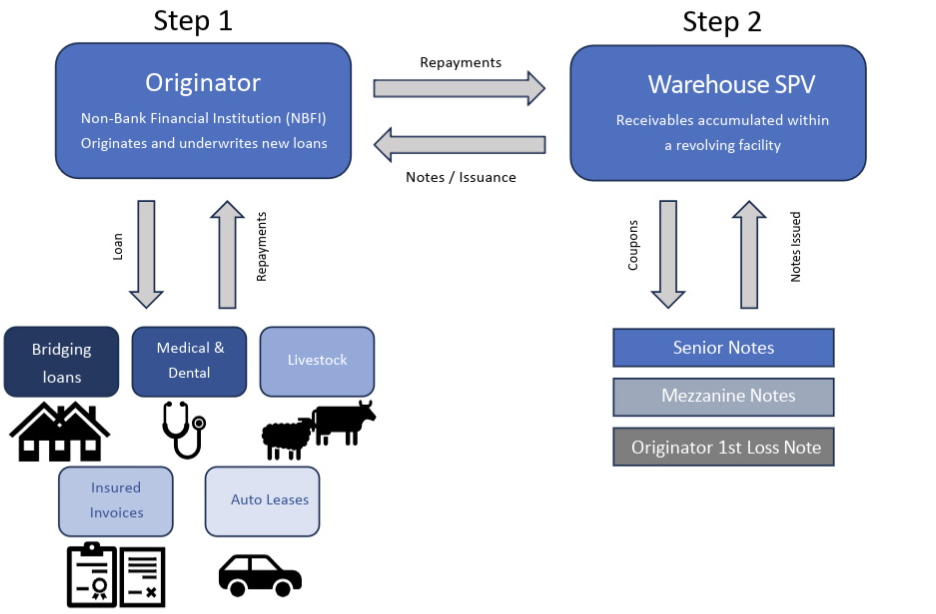

- Loans Are Written: An NBFI makes loans to customers (such as mortgages, leases or invoices).

- Loans Move into a Trust: Each loan is sold in to a separate legal trust(the warehouse).The trust only exists to hold the loans.

- Funding is Provided: Investors fund notes issued by the trust. Their investment is secured against the loans inside the warehouse.

- Borrowers Repay Their Loans:Repayments flow into the trust and are used to:Pay interest to investors, cover costs, and repayfunding.

- Originator Net Interest Margin(NIM): The originator earns income from the difference between the interest paid by borrowers andthe cost of funding the loans

- The Pool Grows Over Time: New loans are added,subject to eligibility. rules and limits based on the providers of capital risk appetite.