In our view, now is an opportune time for investors to use credit, private credit in particular, as an attractive source of income. Given the low interest rate environment and the scarcity of bank dividends, investors should consider an allocation to private credit funds as part of their portfolio composition.

Why is credit potentially attractive as a source of stable income now?

In capital structures, while debt holders do not participate in upside of a business, they do have an interest rate (fixed or floating) linked with funds lent which needs to be paid back at a pre-determined point in time. On the other hand, equity in a business has all the upside but has no guaranteed return or payback. So, in volatile times when revenues decrease and uncertainty prevails, lenders are more likely than equity holders to receive income returns. Given the extreme uncertainty of the Covid-19 induced economic environment, private credit funds are providing particularly interesting opportunities for yield- hungry investors. The search for yield and the ongoing need for income is providing momentum for credit portfolio allocations by investors.

Pre-pandemic growth of private credit funds

Pre-pandemic, a vibrant private credit market had developed in Australia. Traditionally most non-government credit in Australia had been provided by banks in the form of loans. However, as a result of increasing regulatory and cost pressure on the banks, by early 2020 significant growth in private credit markets occurred as banks either withdrew from some sectors or were simply not providing the solutions their clients required. As a result, a substantial non-bank private credit market had been created with the rise of many non-bank / fintech lenders to the Small – Medium size Enterprises (SME’s) and real estate sectors. The size of the non-bank lending market to corporate enterprises exceeded $100bn by the end of 2019. Returns generated varied from the RBA cash rate +3% to in excess of 10% depending on the risk profile of the underlying assets.

How did the pandemic affect the private credit markets?

- The value of private credit returns as a source of stable income became very clear as the pandemic hit. Private credit funds invest in unlisted assets, and as such are not privy to the daily price fluctuations of listed securities that investors had generally relied on for yield, such as equity (generally bank) dividends, real estate investment trusts (REIT’s) and bonds. The Wentworth Williamson Stable Income Fund’s unit price has stayed (and continues to stay) at $1 since its inception. This means that if one had invested $100,000 into the Fund, even throughout the market turbulence experienced in March, the value of this investment stayed at $100,000. To put this into perspective, this was while listed ‘fixed income’ investments suffered significantly reduced returns as the pandemic struck, interest rates were reduced close to zero, real estate rents were placed under immense pressure, and equity dividends to investors were reduced as companies entered survival mode.

- A critical point for investors to address is that, for some time, holding bank term deposits has provided a return below the inflation rate. This became even more acute in Q1 2020 with the reduction in the RBA cash rate to 0.25%. Accessing a credit premium has become essential to produce income returns in excess of inflation for investors.The RBA chart below shows the negative real cash rate that investors have experienced since around 2014 becoming particularly acute in Q1, 2020.

- The banks focused on managing their existing portfolios, creating further space for private credit funds and non-bank lenders

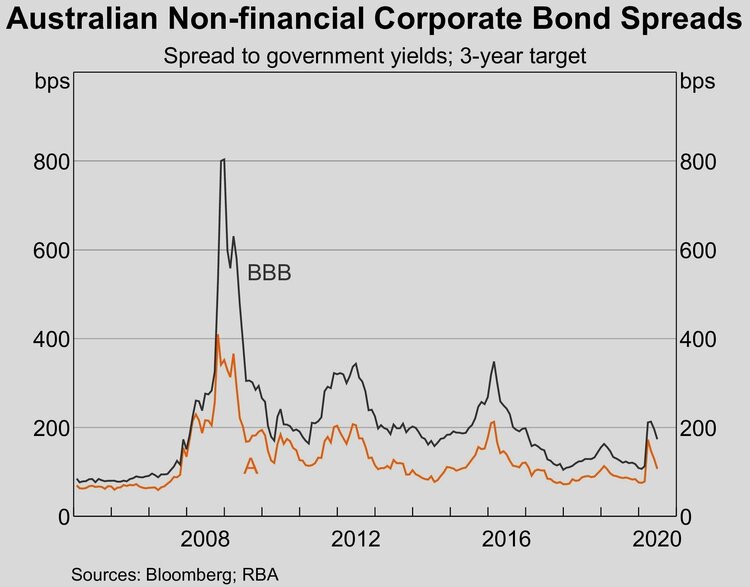

- Market pricing increased, as it always does in times of stressRefer the RBA chart below, which shows the increase in public market A/BBB spreads post pandemic, although not nearly to the same extent as during the 2008 GFC and that there is already a reduction in spreads occurring.

- Many of the underlying borrowers funded by private credit funds did experience stress and did require capital and sometimes interest payments on their loans to be deferred. This was a significant issue for the market but the substantial amount of government fiscal support (at more than 10% of GDP, amongst the highest in the world) provided much needed flexibility to the underlying borrowers via the JobKeeper and many other programs. The Australian government also recognized the importance of the non-bank lending market functioning and allocated $15bn to the Australian Office of Financial Management (AOFM) to assist the non-bank lending market. Nearly $2bn of those funds have now been invested into non-bank lenders primary and secondary and warehouse funding transactions, a meaningful enabler to the credit markets in difficult times.

- Larger corporate borrowers also experienced difficulties but most have been able to restructure their facilities to respond to the pandemic created decrease in their earnings. Successful examples of this include Woodside Petroleum reducing its capital expenditure by 60% and Incitec Pivot holding a successful $675m equity issue and suspending its interim dividend. On the other end of the spectrum, many investors have lost money on the Virgin Australia default, but the Virgin bond issue placed in November last year had exceptionally weak credit metrics and would not have passed the investing requirements of most private credit funds.

Where are the opportunities to generate stable income in private credit now?

Clearly, as with any investing now, caution and careful selection and avoiding following the herd are more important than ever. There are, however, several positive factors for credit fundamentals going forward.

Containment of the virus has been successful, despite the setback by the recent stringent Victoria lockdown. In addition, fiscal spending and monetary support have been and will be extensive for some time. Lastly, businesses and consumers are adapting their capital structures to the new realities.

So, even if the recovery proves to be a swoosh and not a V, we have identified that providing funding to non-bank lenders operating in defined niches with attractive credit histories, are proving to be interesting opportunities for private credit funds to generate stable income for their clients. There are non-bank lenders that have a competitive value proposition against the incumbent banks, have management teams with long and successful track records of providing funding to groups of borrowers that structurally have historically exhibited low historical defaults. An example of this is the funding we provide to a non-bank lender in the medical professional sector – doctors, dentists and vets have been proven to have a high propensity to pay their bills and provide an excellent underlying obligor base for our clients.

For more information on the Wentworth Williamson Stable Income Fund, click here or contact invest@wentworthwilliamson.com.au.