Moral principles aside, shares in companies that produce tobacco products have proved to be very good investments over the years despite the obvious health risks to consumers, constant clamping down by regulators, and an enormous amount of capital remaining unavailable to them due to their lack of ESG credentials. These companies produce enormous amounts of cash flow, they clearly have pricing power and during times of uncertainty or economic downturns will most likely continue to spin out attractive dividends from one year to the next, as they have demonstrated in the past. The analogy to hydrocarbons is used not only because oil and gas producers such as Woodside Energy Group (ASX:WDS) are generating huge amounts of free cashflow at the moment but also because the oil and gas sector has been tarnished with the same brush as social conscious investors did with tobacco stocks. This time environmentalists forced fossil fuel investments into the persona non grata category attempting to starve oil & gas companies of much needed capital and, in some cases, with their activism force a change of strategy to reallocate capital to greener investments. We believe all components of Environmental Social, and Governance (ESG) matrix needs to be given consideration collectively, especially considering that the facts suggest that the death of hydrocarbons in the world’s energy mix has long been greatly exaggerated with some salient facts in the debate been conveniently ignored. Consequently, we think we are now heading down the path to major supply issues which will likely translate to higher prices for longer at a time when the world can least afford it.

Enter the oil & gas sector …

From a moral perspective, we don’t think it’s fair to compare oil & gas producers to tobacco companies. Oil and gas are essential products in every aspect of our lives. Humankind has benefitted enormously from the downstream applications such as fertilisers, plastics, clothing, lubricants, and transport to name a few; since the discovery of these applications in the nineteenth century, the world’s population grew from ~1 to ~8 billion. Although some of these uses can be replaced in time (and we hope they are) there are some downstream applications that will continue to persist long into the future.

It is likely low energy and capital costs contributed significantly to the cost reduction in wind and solar between 2010 and 2020. During this period, we not only travelled through the lowest cost of capital in our lifetimes but the input prices of all other forms of energy commodities such as gas, oil, coal, and uranium remained low as well. Contrary to popular opinion, wind and solar are extremely energy-intensive forms of power. For example, per MW the average wind turbine uses about 345 tonnes of concrete, 120 tonnes of steel, 5 tonnes of plastics (oil), 8 tonnes of glass, 20 tonnes of iron, 5.5 tonnes of zinc and almost 10 tonnes of other elements like copper, manganese, nickel, and chromium to name a few. These materials require huge amounts of energy to mine, process and refine. Over the last decade or so these commodities have been extracted at relatively low cost and projects could be financed at low rates right from the mine through to the development of the wind farm. Even before we start to estimate a significantly higher new normal cost for renewable energy sources, it has been estimated that with battery storage, the average windfarm produces energy returned on energy invested (EROEI) of 4:1, compared with 30.1 for traditional hydrocarbons.1

1for every 1 unit of energy you put into a wind farm you will get 4 back. For every 1 unit of energy you put into extracting hydrocarbons you will get 30 back

To be clear, we also want growth in renewable energy and significant capital made available for innovation as climate change is an important issue to us. However, as illustrated above, the investment community has not been comparing apples with apples and it should now be obvious that the transition to renewables needs to occur at a sensible pace considering the ‘S’ for social factors to consider in ESG. Additionally, we think some capitalists have had a field day with their greenwashing initiatives, and perhaps many just believed it because it was the consensus at the time. As a result, we are now facing significantly higher energy costs not only from traditional fossil fuels but most likely from renewable energy sources as well.

Twenty years ago, the ‘peak oil’ debate was alive and well and the consensus at the time was that we needed to invest in higher cost projects as production rates of conventional oil sources appeared to be reaching a production plateau -. The expectation was that the oil price would keep increasing over time as we travelled up the global oil & gas cost curve.

So what happened …?

New technology in the US with fracking technology, particularly horizontal drilling, came to the ‘rescue’ temporarily. This oil was still costlier than conventional sources as production from individual wells declined rapidly, necessitating constant drilling which naturally increased costs. However, drunk on cheap finance, US-based frackers went deeply into debt drilling thousands of holes into Texas, North Dakota, and a few other states. US production started to increase in 2008 and over the next seven years marked the fastest oil production increase in U.S. history. The country became the largest oil producer in the world flooding global oil supply. As a result, the oil price weakened significantly and this in turn wiped out many equity investors in the US fracking industry, as they were still relatively high on the global cost curve. At the same as this was happening in the US fracking industry, environmentalists’ laser-like focus on climate change has resulted in capital expenditure to be at its lowest level since 2007 (except for the COVID years).

Over the last decade ESG investors significantly curtailed investment in the oil & gas sector. We highlight in the points below some of the extreme pressure executives and non-executives of the oil & gas majors have faced from ESG investors in recent years. This is by no means an exhaustive list but should help to illustrate why we are staring down a supply crisis today. At a time when we need the energy sector to perform, its weighting in the MSCI Global Index has more than halved over the last decade from 10.7% to 4.4%.

- In 2021 despite barely controlling any of Exxon’s shares, activist investors control a quarter of Exxon’s board seats. They are looking to scale back production targets and focus on new green technologies. After this meeting Chevron announced a $3bn bio-diesel investment which has terrible financial economics, compared to what they would have achieved investing in an oil and gas project

- In 2021 a Dutch court ordered that Shell must reduce global net carbon emissions by 45% by 2030 compared with 2019. Now they are under pressure to split the company into two and redirect all profits to the second company which will hold the renewable investments

- The CEOs of Exxon, Chevron, Shell and BP have been dragged before Congress numerous times (the most recent on 15th September 2022) to be criticised for disinformation about climate change and for not doing more to restrict investment in new fossil fuel projects. At the same Joe Biden has threaten oil companies with ‘emergency powers’ if they do not increase supply

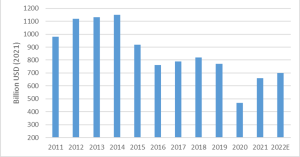

The ESG push at all costs is having an effect. Spending on new projects has reduced dramatically and production from the majors has been declining. Additionally new sources of oil and gas are getting harder to find as the ‘easy and cheap’ discoveries usually come first so $1 spent on exploration today is less and less likely to strike a new discovery. It is now more than likely that there is insufficient investment available to counter the natural depletion of existing resources. See figure 1 below, Investment in new oil and gas sources is 30-40% below 2011-2016 levels. This number should be increasing to offset increasing natural depletion rates.

Figure 1: Global Investment in Fuel Supply

Source: International Energy Agency, World Energy Investment 2022

Conventional oil production has plateaued. Another key factor why we believe the World is heading towards a period of higher energy prices for longer is that it is becoming increasingly evident that Saudi Arabia does not have the spare capacity that everyone thought it had. In response to political pressure after the Russian invasion of Ukraine, Saudi Arabia promised to increase production to 13 million barrels per day. They have never achieved this production level and are not even coming close to this level currently.

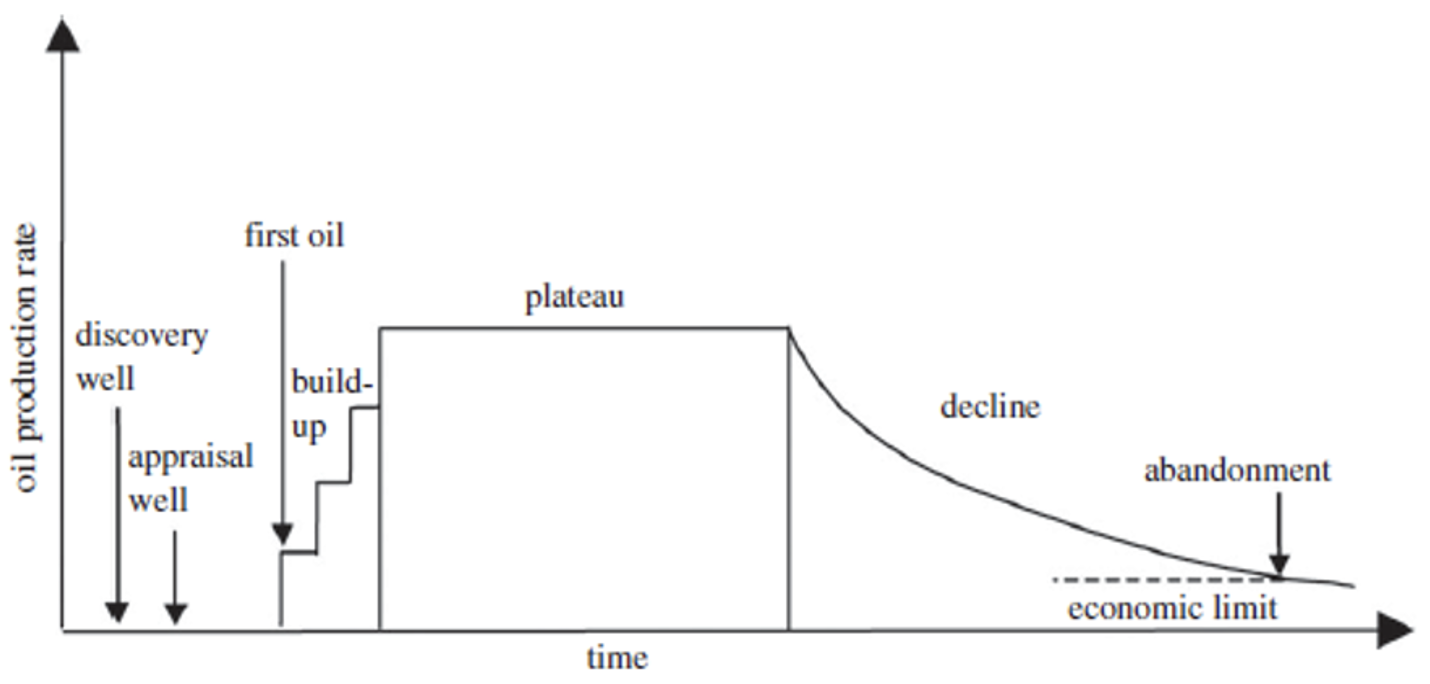

Conventional oil is essentially oil that can be extracted using traditional drilling methods and that can flow at surface temperature and pressure conditions naturally. It is oil low on the cost curve and it includes the massive Ghawar oilfield in Saudi Arabia. And herein lies another major problem. Marion King Hubbert a renowned oil geologist with Shell came up with a theory that has been proven right time and time again that an oilfield reaches peak production after half of its reserves have been produced. The lifecycle of a typical conventional oil field is represented in figure 2 below.

Figure 2: The lifecycle of a conventional oil field

Source: Höök M, Davidsson S, Johansson S, Tang X.

The point we are making is that there is increasing evidence that we may have already reached peak production rates for the world’s conventional oil reserves, including for the massive Ghawar oilfield in Saudi Arabia. Put another way, we have already extracted half of the world’s low-cost oil already and it may now be technically impossible to materially increase production rates for these reserves. Saudi Arabia may be demonstrating this point right now, despite pressures from the U.S. and the rest of the world to increase production.

We have put a large emphasis on the reasons why we believe we are staring down the barrel of an oil & gas supply crisis and have not elaborated on the demand side in this report. However, on the 14th of March 2022 we published a report which addresses our opinion as to why the demise of demand for oil & gas demand is greatly exaggerated, see link here https://wentworthwilliamson.com.au/insights/our-view-on-oil-and-gas-prices/.

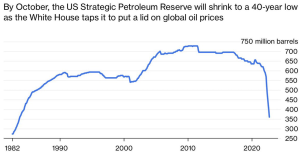

In recent weeks oil & gas prices have retreated on recession fears and as can be seen from figure 3 below, the Biden administration is making best efforts to put a lid on inflation by selling down their Strategic Petroleum Reserves. However, over the next several years we believe oil & gas demand will remain at around current levels or post some modest growth. The real challenge will be meeting this demand with an adequately priced supply. Unfortunately, we conclude that we believe consumers around the world will need to get used to paying higher prices for their energy, unless governments around the world take to huge subsidisation, which has its separate dangerous economic implications.

Figure 3: Oil Piggy Bank

Source: US Department of Energy

June-Oct 2022 is forecast based on releases already pre-announced

The Wentworth Williamson Fund owns the following stocks that stand to benefit, either directly or indirectly, from elevated oil & gas prices over the next several years:

- Woodside Petroleum Limited (ASX:WPL) – Australia’s blue chip gas producer.

- MRM Offshore (ASX:MRM) – an offshore oil, gas and wind service provider.

- Fleetwood Limited (ASX:FWD) – Owns a fly-in-fly-out hotel in the soon to be ‘boom time’ Karratha city in Western Australia due to the massive Scarborough and downstream developments in the region.

Sources

https://www.nytimes.com/2021/06/09/business/exxon-mobil-engine-no1-activist.html

https://www.msci.com/documents/1296102/28995615/MSCI-_-Impact-_-ACWI-IMI-sector-breakdown.pdf

Source: Goehring & Rozencwajg

https://festkoerper-kernphysik.de/Weissbach_EROI_preprint.pdf

https://eitrawmaterials.eu/wp-content/uploads/2020/04/rms_for_wind_and_solar_published_v2.pdf

https://iea.blob.core.windows.net/assets/db74ebb7-272f-4613-bdbd-a2e0922449e7/WorldEnergyInvestment2022.pdf

https://www.msci.com/documents/1296102/28995615/MSCI-_-Impact-_-ACWI-IMI-sector-breakdown.pdf